Initially-residence purchaser sector complexity unveiled | Australian Broker News

Information

Very first-house purchaser trade complexity unveiled

CoreLogic particulars reveals nuanced entry challenges

Eliza Owen (pictured increased than), head of family examine Australia at CoreLogic, analysing Ab muscle groups housing finance data, underscored the escalating problem confronted by initial-house potential patrons in Australia’s hovering true property trade.

Irrespective of a sizeable enhance within the CoreLogic House Value Index by someplace round 150% in regards to the earlier two a few years, wages haven’t saved price, rising solely 82% in accordance to the Abdominal muscle groups Wage Rate Index.

The disparity has widened the opening in home affordability for initially-time shoppers, mirrored by “a deterioration in affordability metrics and an improve within the widespread age of very first property purchasers about time.”

Misleading surge in finance

Whilst the ABS’ lending indicators data from February confirmed a substantial $4.9 billion secured by 1st-household potential patrons, up 4.8% from the sooner thirty day interval, the determine doesn’t essentially point out improved accessibility.

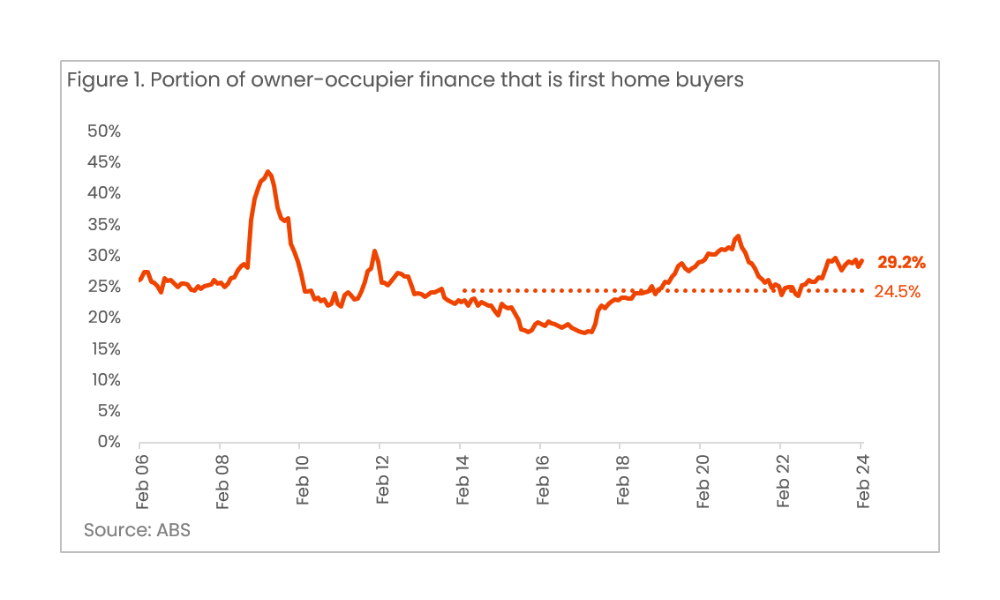

The data may probably counsel initial-dwelling potential patrons are beginning to be a bigger sized portion of the market place with 29.2% of all operator-occupied finance, however as Owen identified, “Does this suggest first-household potential patrons are getting it easier to buy dwelling? Not robotically.”

Contextualising finance development

The enhance in 1st-dwelling client finance is contrasted by the slower enlargement or decline in non-very first-dwelling client finance, skewing the all spherical picture. Over the sooner 12 months, the value of very first-property client lending has surged by 20.7%, quadrupling the annual improvement payment of non-very first family purchaser proprietor-occupier lending, which stands at 5%.

“The maximize within the share of 1st-property purchaser finance has been exacerbated by comparatively delicate improvement in non-very first-property purchaser proprietor occupier finance,” Owen acknowledged.

The relative measurement indicated rather more in regards to the trade dynamics than a official enhance in initial-household buyer participation.

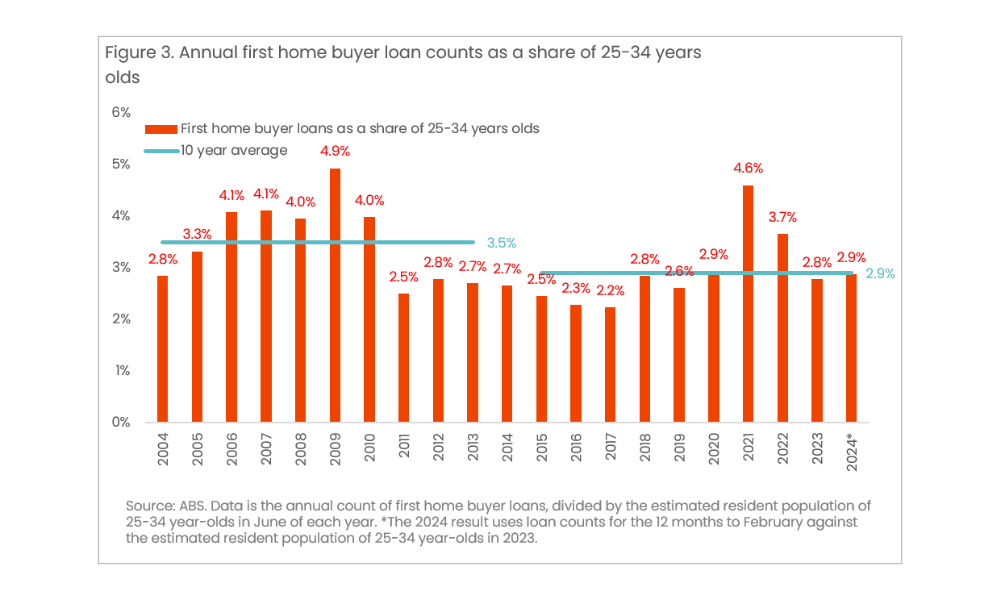

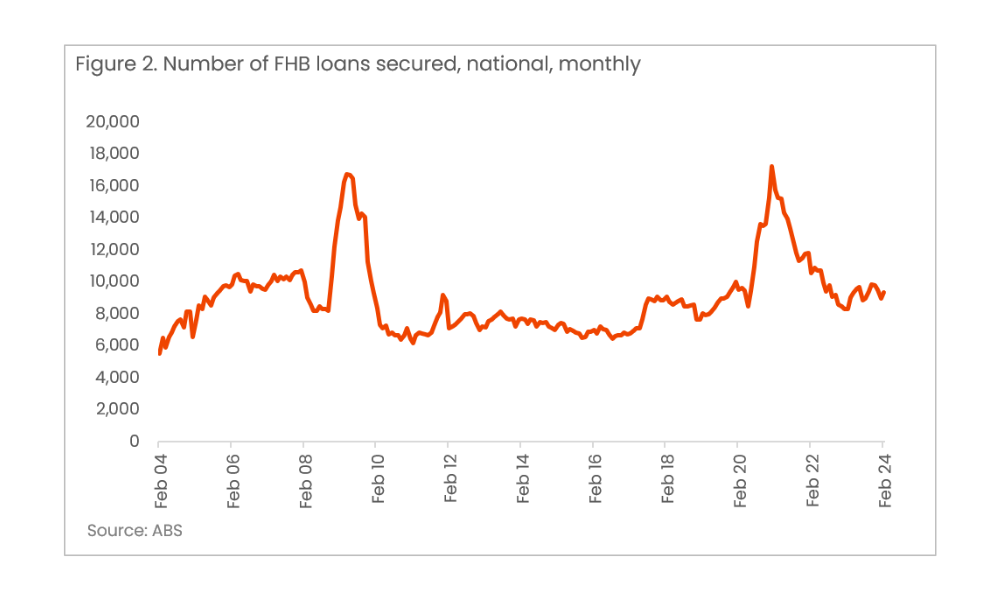

Actual image of very first-residence client loans

Despite appearances, the exact vary of to begin with-dwelling client loans secured is right now beneath the historical past massive of 2021, with appreciable fluctuations primarily attributed to short-term federal authorities incentives.

This cyclical pattern fails to produce a steady foundation for sustained 1st-house client market entry, primarily when enthusiastic about the broader monetary panorama impacting dwelling values and market competitiveness.

Impression of federal authorities incentives

Short-term govt incentives this sort of because the initially dwelling operator grant and the HomeBuilder grant have traditionally made spikes in first-home client motion. On the opposite hand, these are considered as artificial boosts that don’t give you long-term help or affordability.

“These grants appear to be to have a short-term consequence on to begin with-dwelling buyer figures and should probably simply carry ahead want for all those who may have purchased into the market place at a in a while day,” Owen defined.

Get one of the best and freshest mortgage mortgage information despatched proper into your inbox. Subscribe now to our FREE day by day e-newsletter.

Continue to maintain up with probably the most present data and occasions

Be a part of our mailing file, it’s free!